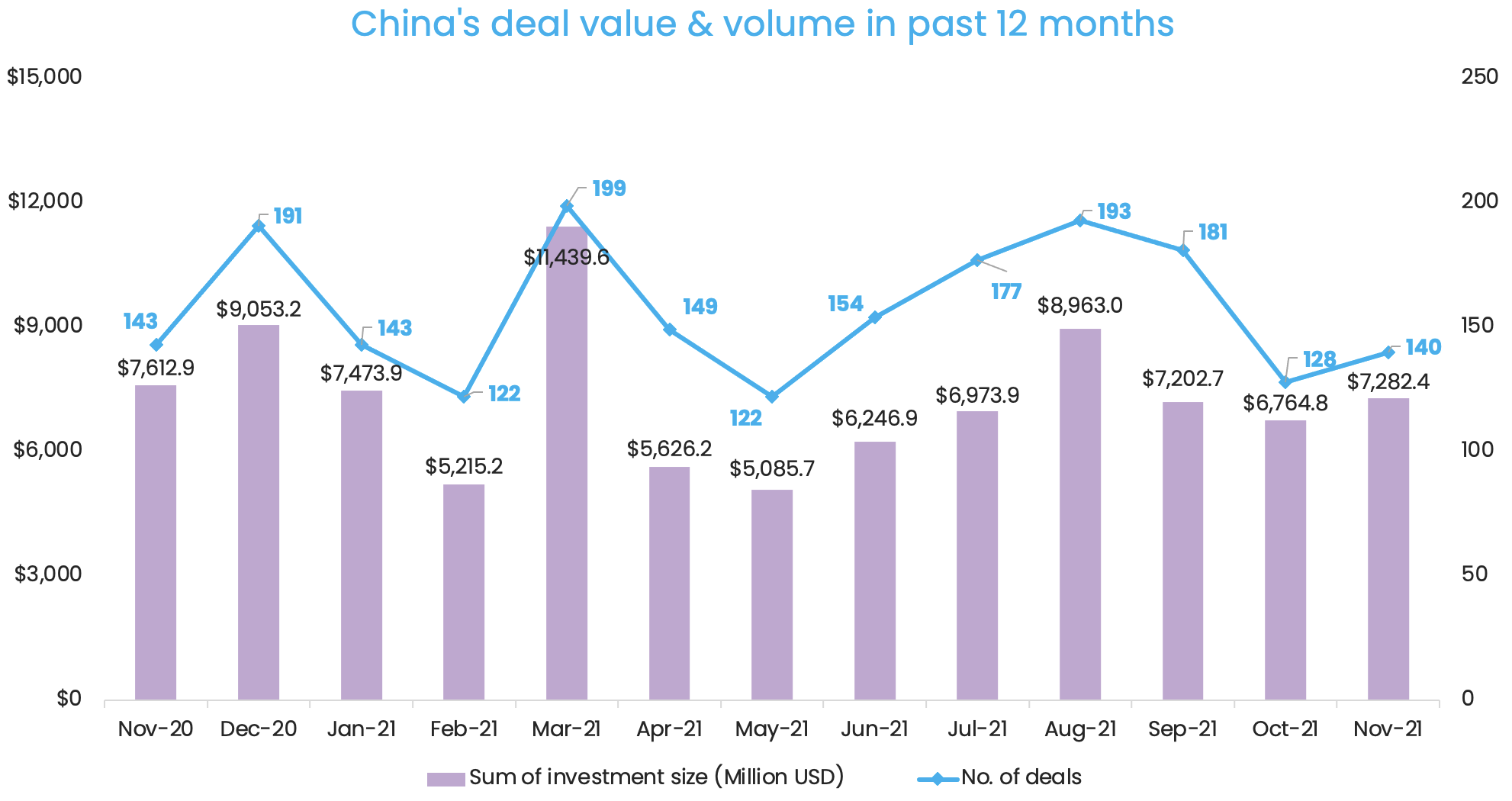

Startups in the Greater China region raised nearly $7.3 billion across 140 private equity (PE) and venture capital (VC) deals in November.

The deal count was an increase of 9.4% from October, while total deal value also grew by 7.7% month-on-month, according to proprietary data compiled by DealStreetAsia.

However, dealmaking activity showed less vitality compared with November 2020 when Greater China startups collected $7.6 billion across 143 PE-VC deals. In the past month, the aggregate startup funding was down 4.3% year-over-year (YoY). The deal count fell 2.1% from November 2020.

The monthly investment size was propped up by two billion-dollar deals: In November’s largest funding round, GTA Semiconductor, a developer of intelligent integrated circuits (ICs) for applications in areas like auto electronics and power management, raked in 8 billion yuan ($1.26 billion). Chinese IC design house Huada Semiconductor led the round, with participation from investors including Cathay Capital.

Greentech player Envision Group closed the second-biggest financing. The provider of renewables, hydrogen, battery, and digital solutions attracted an investment of over $1 billion from Sequoia Capital China, Singapore sovereign wealth fund GIC, and Primavera Capital. In October, the firm’s subsidiaries, Envision Energy and Envision AESC, collectively raised over $600 million.

November also saw the completion of a $500-million deal by Momenta. The autonomous driving startup raised fresh capital in an extended Series C round from investors including US automaker General Motors, Singapore state investor Temasek Holdings, and Japan’s Toyota Motor Corp. The deal followed a $300-million financing in September and a $500-million financing in March, bringing the size of the Series C round to over $1 billion.

Megadeal funding upsizes

Besides the investments in GTA, Envision, and Momenta, several sizeable megadeals contributed to the bulk of the capital raised in the month.

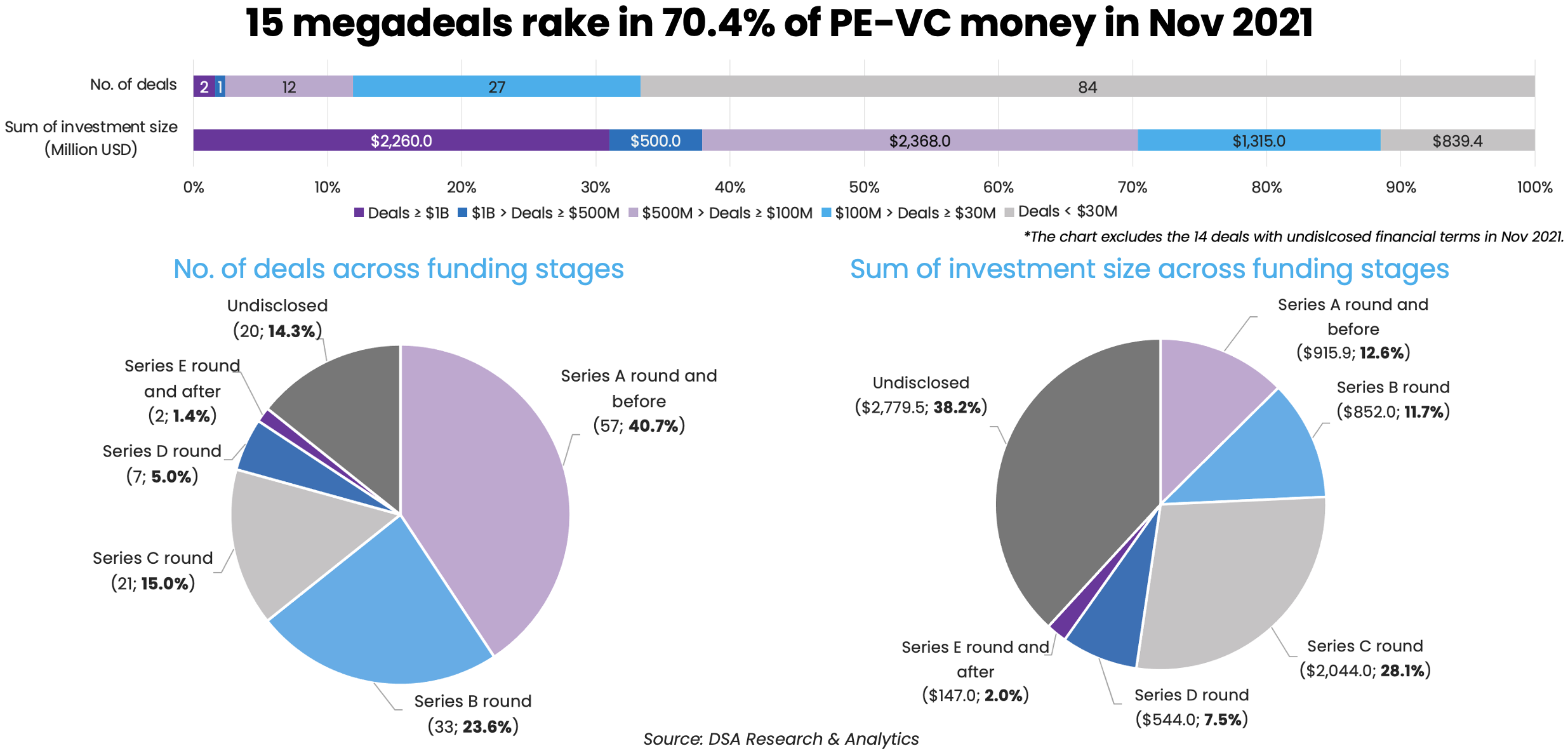

Fifteen megadeals, which refer to investments worth atleast $100 million, gathered over $5.1 billion in November. The total value of these megadeals was 8.5% more than that in the previous month, when 15 megadeals amassed just over $4.7 billion.

The megadeals in November accounted for 70.4% of the total funding. This share had stood at 69.6% in October, 62.7% in September, and 67.2% in August.

The value of 12 megadeals fell within the range of $100-500 million ($100 million inclusive). They attracted renowned investors, such as SoftBank Group Corp, Sequoia Capital China, KKR & Co, and Goldman Sachs, to make bets on industries ranging from biotech and insurance to the internet and software.

Startups in their earlier funding stages completed more deals than their growth- and late-stage counterparts. Fundraisers in the Series A round and earlier led the pack with 57 deals, or 40.7% of the month’s total deal count. Deal count at the Series B stage followed with 33 deals.

Less than one-quarter of transactions were made at the growth- and late-stage with 21 Series C deals, seven Series D deals, and two deals at Series E round and after.

Investors made bold bets on Series C deals since over $2 billion, or 28.1% of the month’s financing, flowed into fundraisers at the stage. It also reflected on the composition of megadeals — seven of the 15 largest investments of $100 million and over happened at the Series C stage.

The aggregate deal value at the Series A stage came second, at $915.9 million, followed by that of the Series B stage, Series D stage, and Series E stage.

List of 15 megadeals in Nov 2021

Startup

Headquarters

Investment size (USD)

Investment stage

Lead investor(s)

Investor(s)

Industry

Vertical

GTA Semiconductor

Shanghai

$1,260 million

Cathay Capital

Semiconductor

CleanTech

Envision Group

Shanghai

$1,000 million

Strategic investment

Sequoia Capital, GIC Private Ltd, Primavera Capital

Renewable Energy

CleanTech

Momenta

Beijing

$500 million

C+

General Motors, Temasek, Bosch, Toyota, SAIC Motor, Yunfeng Capital

Auto & Parts

Autonomous Driving

Hesai Technology

Shanghai

$370 million

D

Xiaomi Corporation, GL Ventures, Meituan, CPE, Xiaomi Industry Investment

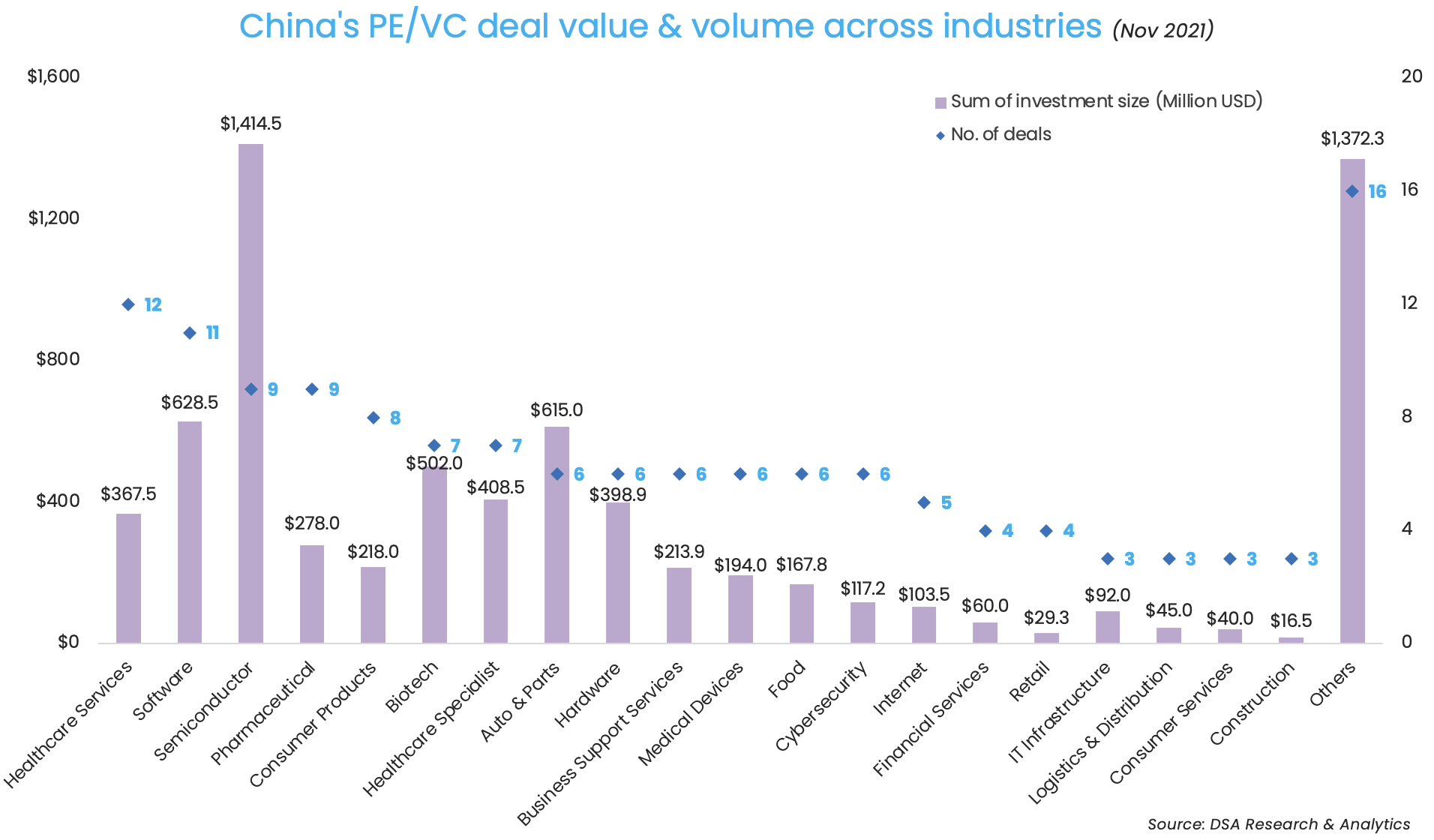

Investments in China’s semiconductor startups are heating up, as the government ramps up efforts to achieve technology self-reliance amid its trade tensions with the US. Startup funding in the field topped in November, with over $1.4 billion being raised across nine deals.

While the deal count increased, compared with six in October, it is important to note that $1.26 billion, or 90% of the capital in the field, came from GTA’s new round. The remaining money was largely raised across deals of lower than $50 million, except for North Ocean Photonics’ Series B+ round that is worth close to 400 million yuan ($63 million).

Financing in the semiconductor industry is expected to grow as the global chip shortage drags on. Tech-market researcher Gartner Inc projects global chip manufacturers to pour about $146 billion into capital expenditures in 2021. That would be an approximately one-third increase from 2020 and 50% higher than 2019. That investment would be more than double the industry spending of five years ago.

Healthcare services led the pack in terms of deal count. PE-VC investments in the area outnumbered all other industries with the completion of 12 deals in the month. The biggest fundraiser was Tripod, a contract research organisation (CRO) that closed a new round of nearly 1 billion yuan ($155 million) led by China’s Ruihua Investment Management, Lilly Asia Ventures, and GL Ventures.

Another two healthcare services providers sealed sizeable deals, namely Jianhai Technology, which raised 500 million yuan ($78 million) in a Series B+ round, and Landing Med, which completed a Series D round of 320 million yuan ($50 million).

Sequoia China is top investor

Sequoia Capital China, the bellwether of tech investments in China, retained its perch on top as the most active investor in Greater China with participation in at least 11 deals worth a combined $1.5 billion.

Sequoia China was created in 2005 by Neil Shen as the China franchise of Silicon Valley’s Sequoia Capital. The firm has invested in about 600 companies over the past 16 years, including some of China’s biggest tech firms like e-commerce giants Alibaba and JD.com, food delivery firm Meituan, and ride-hailing service provider Didi Global.

Matrix Partners China, affiliated with Matrix Partners in the US, ranked second with participation in seven deals. The total value of Matrix China-backed deals only reached $198 million, because six of the seven investments were small-cheque deals at the early funding stage of Series A round or earlier.

It only invested in one growth-stage deal, namely a $150-million Series C round in Cyclone Robotics, a developer of robotic process automation (RPA) software.

ByteDance investor Source Code Capital and Shunwei Capital, which is backed by smartphone brand Xiaomi’s founder Lei Jun, were tied for third place. Other active investment firms in October were Hillhouse Capital’s VC arm GL Ventures, Xiaomi, and early-stage venture firm GSR Ventures.

Most active investors in China’s PE-VC market (Nov 2021)

Investment company

No. of deals

Total value of participated deals (USD)

Lead

Non-lead

Sequoia Capital China

11

$1,537 million

6

5

Matrix Partners China

7

$198 million

4

3

Source Code Capital

6

$571 million

4

2

Shunwei Capital

6

$36 million

4

2

GL Ventures

5

$410 million

3

2

Xiaomi and affiliates

5

$395 million

3

2

GSR Ventures

5

$105.5 million

2

3

ZWC Partners

4

$401.5 million

2

2

GGV Capital

4

$189.7 million

3

1

Plum Ventures

4

$15.5 million

1

3

*If one deal is backed by only two investors, we consider neither of the two investors as a lead investor.

Liya Su contributed to the story.

Note: In our monthly analysis for November 2021, we have put together detailed charts of prominent deals, active investors, deal stages, and the most attractive sectors that have bagged the maximum venture dollars in the Greater China region.

Our database only considers deals officially announced by the related investee, investor(s), and/or financial advisor, while information based on market rumours and news reports citing sources is excluded.

For a more detailed analysis, and to enable comparison between primary and secondary markets, DealStreetAsia has started tracking deals of all sizes since April 2020, as against considering only transactions worth more than $10 million earlier.

We have also introduced a standardised system for industry classification. It currently includes over 50 industries, as well as over 45 new economy and high-tech verticals, which will progressively increase to adapt to local market conditions in our closely watched regions of Greater China, Southeast Asia, and India.

Share this story with your friends and colleagues.

DealStreetAsia Partner Content

‘In an era of virtual dealmaking, stakeholders tend to be more transparent’ – DFIN’s Peter McMillan

Over half the deals in the next 3 months will be hosted virtually according to 79% of the respondents in DFIN’s DealMaker Meter Survey. Peter McMillan, Head of Sales for APAC at DCIN speaks of the advantages of virtual dealmaking as well as the pitfalls to be avoided, in an exclusive interview with DealStreetAsia

The startup fraternity in Southeast Asia has reasons to cheer. Even as the adverse impacts of the COVID-19 pandemic are still...

Read the Report

The Deals Barometer is brought to you by

We use cookies to help us better understand your experience of our site. The information we collect is used to measure and improve performance, and to better understand your needs. We may share this data with our hosting, advertising and analytics partners. Cookie Policy

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.